Call:

lm(formula = median_incomeE ~ total_popE, data = pa_data)

Residuals:

Min 1Q Median 3Q Max

-39536 -6013 -1868 5075 44196

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 62855.819808 1760.477709 35.704 < 0.0000000000000002 ***

total_popE 0.021477 0.005192 4.137 0.000103 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 11820 on 65 degrees of freedom

Multiple R-squared: 0.2084, Adjusted R-squared: 0.1962

F-statistic: 17.11 on 1 and 65 DF, p-value: 0.0001032Introduction to Linear Regression

Week 5: MUSA 5080

Dr. Elizabeth Delmelle

2025-10-06

Opening Question

Scenario: You’re advising a state agency on resource allocation.

Some counties have sparse data. Can you predict their median income using data from counties with better measurements?

Broader question: How do we make informed predictions when we don’t have complete information?

Today’s Roadmap

- The Statistical Learning Framework: What are we actually doing?

- Two goals: Understanding relationships vs Making predictions

- Building your first model with PA census data

- Model evaluation: How do we know if it’s any good?

- Checking assumptions: When can we trust the model?

- Improving predictions: Transformations, multiple variables

Part 1: The Statistical Learning Framework

The General Problem

We observe data: counties, income, population, education, etc.

We believe there’s some relationship between these variables.

Statistical learning = a set of approaches for estimating that relationship

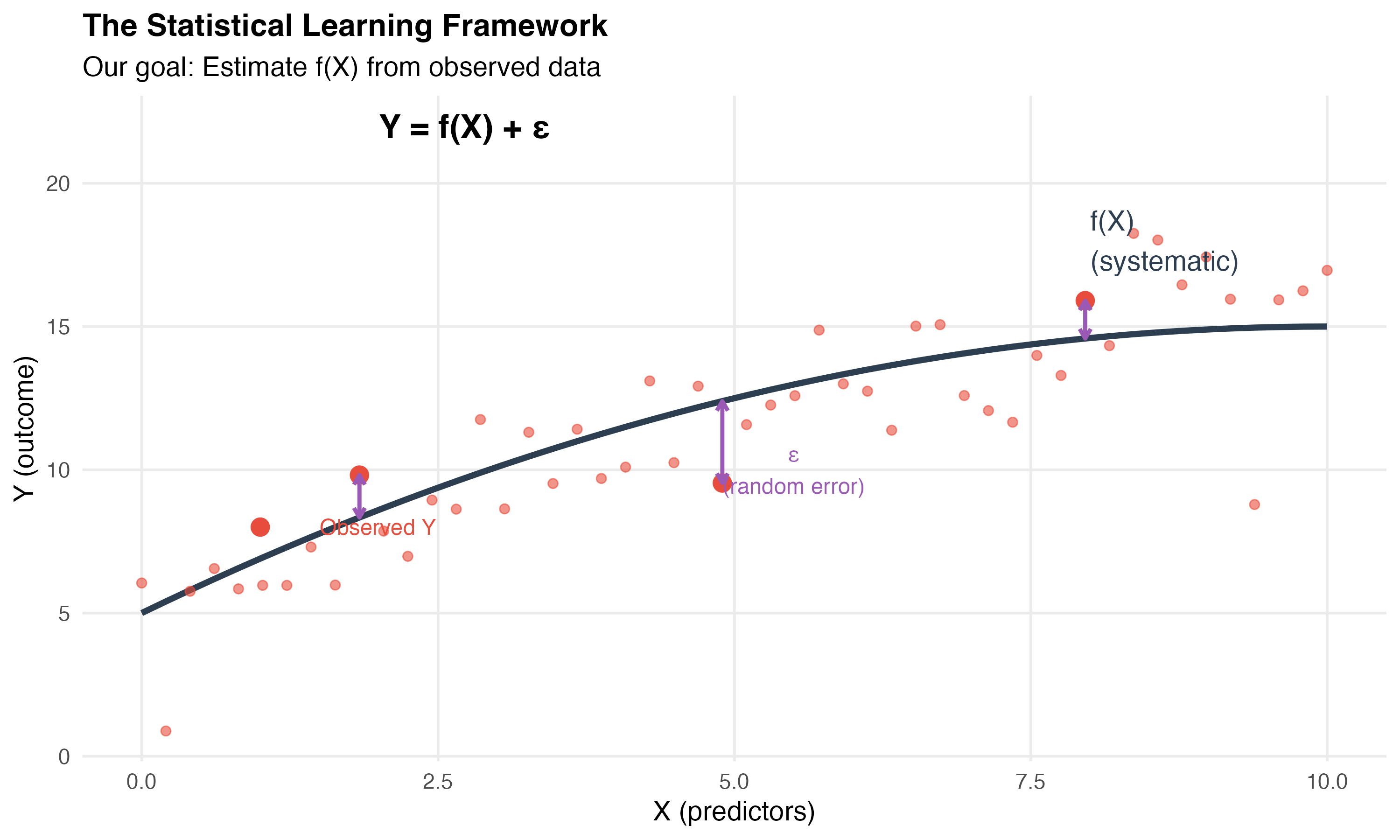

Formalizing the Relationship

For any quantitative response Y and predictors X₁, X₂, … Xₚ:

\[Y = f(X) + \epsilon\]

Where:

- f = the systematic information X provides about Y

- ε = random error (irreducible)

What is f?

f represents the true relationship between predictors and outcome

- It’s fixed but unknown

- It’s what we’re trying to estimate

- Different X values produce different Y values through f

Example:

- Y = median income

- X = population, education, poverty rate

- f = the way these factors systematically relate to income

Why Estimate f?

Two main reasons:

1. Prediction

- Estimate Y for new observations

- Don’t necessarily care about the exact form of f

- Focus: accuracy of predictions

2. Inference

- Understand how X affects Y

- Which predictors matter?

- What’s the nature of the relationship?

- Focus: interpreting the model

How Do We Estimate f?

Two broad approaches:

Parametric Methods

- Make an assumption about the functional form (e.g., linear)

- Reduces problem to estimating a few parameters

- Easier to interpret

- This is what we’ll focus on

Non-Parametric Methods

- Don’t assume a specific form

- More flexible

- Require more data

- Harder to interpret

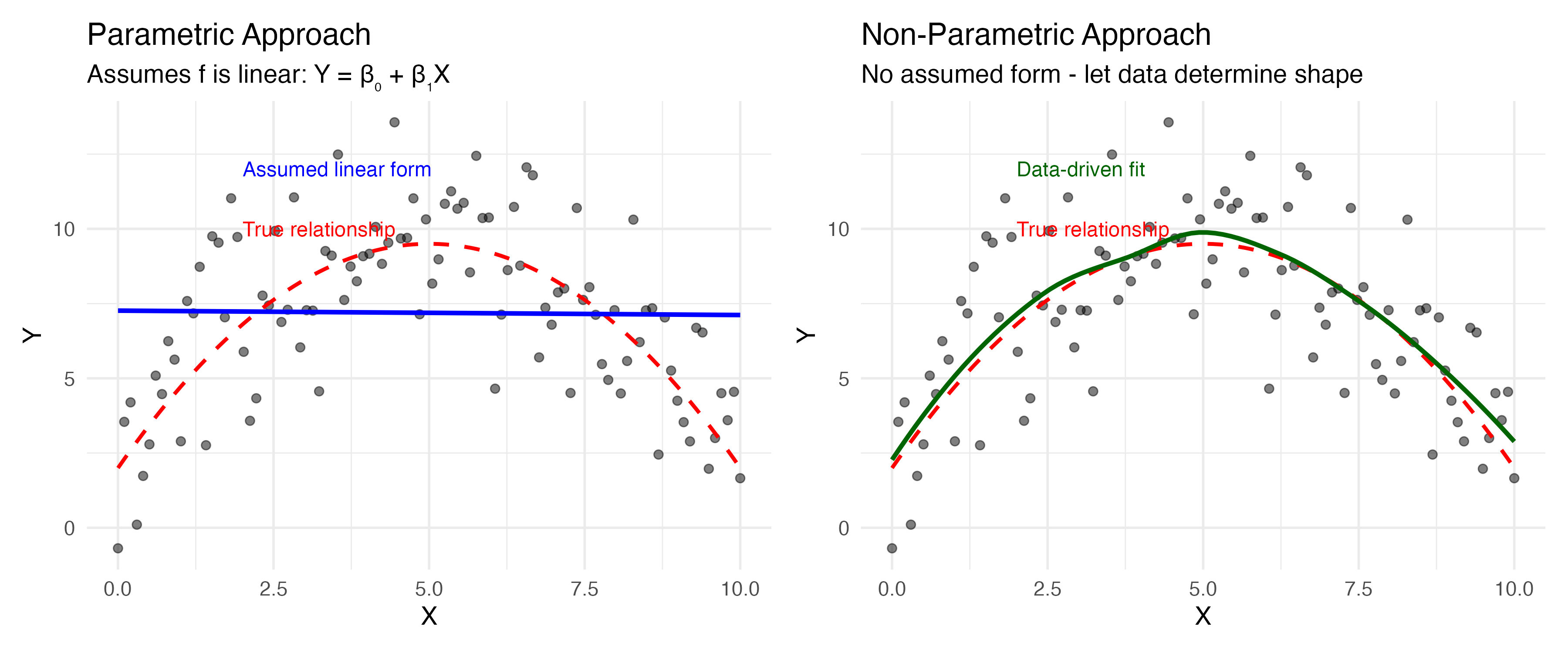

Parametric vs. Non-Parametric

Key difference:

- Parametric (blue): We assume f is linear, then estimate β₀ and β₁

- Non-parametric (green): We let the data determine the shape of f

What about deep learning?

Neural networks are technically parametric (millions of parameters!), but achieve flexibility through parameter quantity rather than assuming a rigid form. We won’t cover them in this course, but they follow the same Y = f(X) + ε framework.

Parametric Approach: Linear Regression

The assumption: Relationship between X and Y is linear

\[Y \approx \beta_0 + \beta_1X_1 + \beta_2X_2 + ... + \beta_pX_p\]

The task: Estimate the β coefficients using our sample data

The method: Ordinary Least Squares (OLS)

Why Linear Regression?

Advantages:

- Simple and interpretable

- Well-understood properties

- Works remarkably well for many problems

- Foundation for more complex methods

Limitations:

- Assumes linearity (we’ll test this)

- Sensitive to outliers

- Makes several assumptions (we’ll check these)

Part 2: Two Different Goals

Prediction vs Inference

The same model serves different purposes:

Inference

- “Does education affect income?”

- Focus on coefficients

- Statistical significance matters

- Understand mechanisms

Prediction

- “What’s County Y’s income?”

- Focus on accuracy

- Prediction intervals matter

- Don’t need to understand why

Today: We’ll do both, but emphasize prediction

Example: Prediction

Government use case:

Census misses people in hard-to-count areas. Can we predict:

- Income for areas with poor survey response?

- Population for planning purposes?

- Resource needs based on demographics?

The model doesn’t explain WHY these relationships exist, but if predictions are accurate, they’re useful for policy

Example: Inference

Research use case:

Understanding gentrification:

- Which neighborhood characteristics explain income change?

- How much does education matter vs. proximity to downtown?

- Are policy interventions associated with outcomes?

Here we care about the coefficients and what they tell us about mechanisms

Connection to Week 2: Algorithmic Bias

Remember the healthcare algorithm that discriminated?

The model: Predicted healthcare needs using costs as proxy

Technically: Probably had good R², low prediction error (good “fit”)

Ethically: Learned and amplified existing discrimination

Critical Point

A model can be statistically “good” while being ethically terrible for decision-making.

Part 3: Building Your First Model

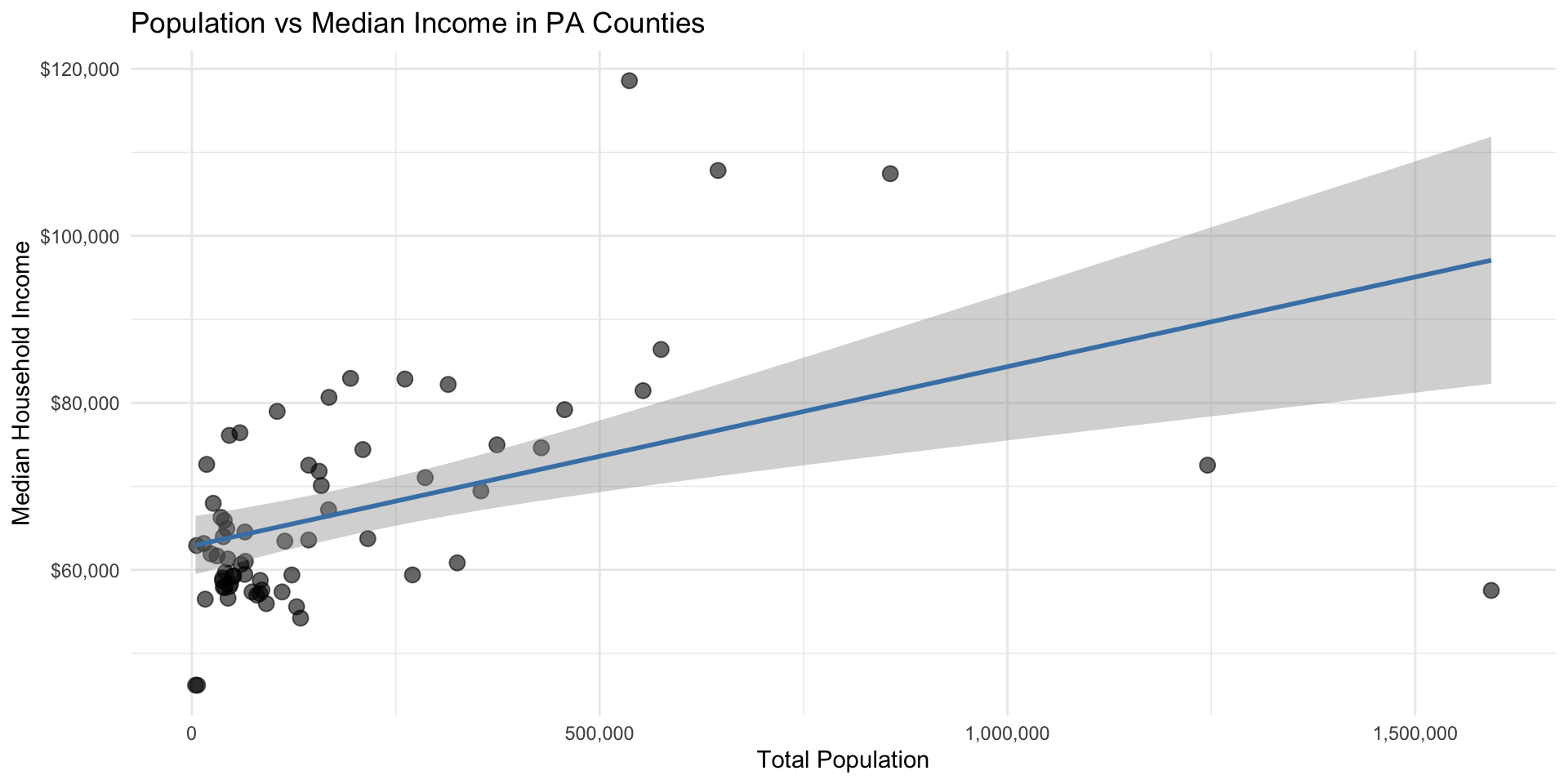

Start with Data and Visualization

Let’s apply these concepts to PA counties:

What Do We See?

Before fitting any model, discuss the visualization:

- Generally positive relationship

- Considerable scatter (not deterministic)

- Most counties are small (clustered left)

- One large county with surprisingly low income

- Wider confidence band at higher populations

Question: What does this tell us about f(X)?

Fit the Model

Interpreting Coefficients

Intercept (β₀) = $62,855

- Expected income when population = 0

- Not usually meaningful in practice

Slope (β₁) = $0.02

- For each additional person, income increases by $0.02

- More useful: For every 1,000 people, income increases by ~$20

Is this relationship real?

- p-value < 0.001 → Very unlikely to see this if true β₁ = 0

- We can reject the null hypothesis

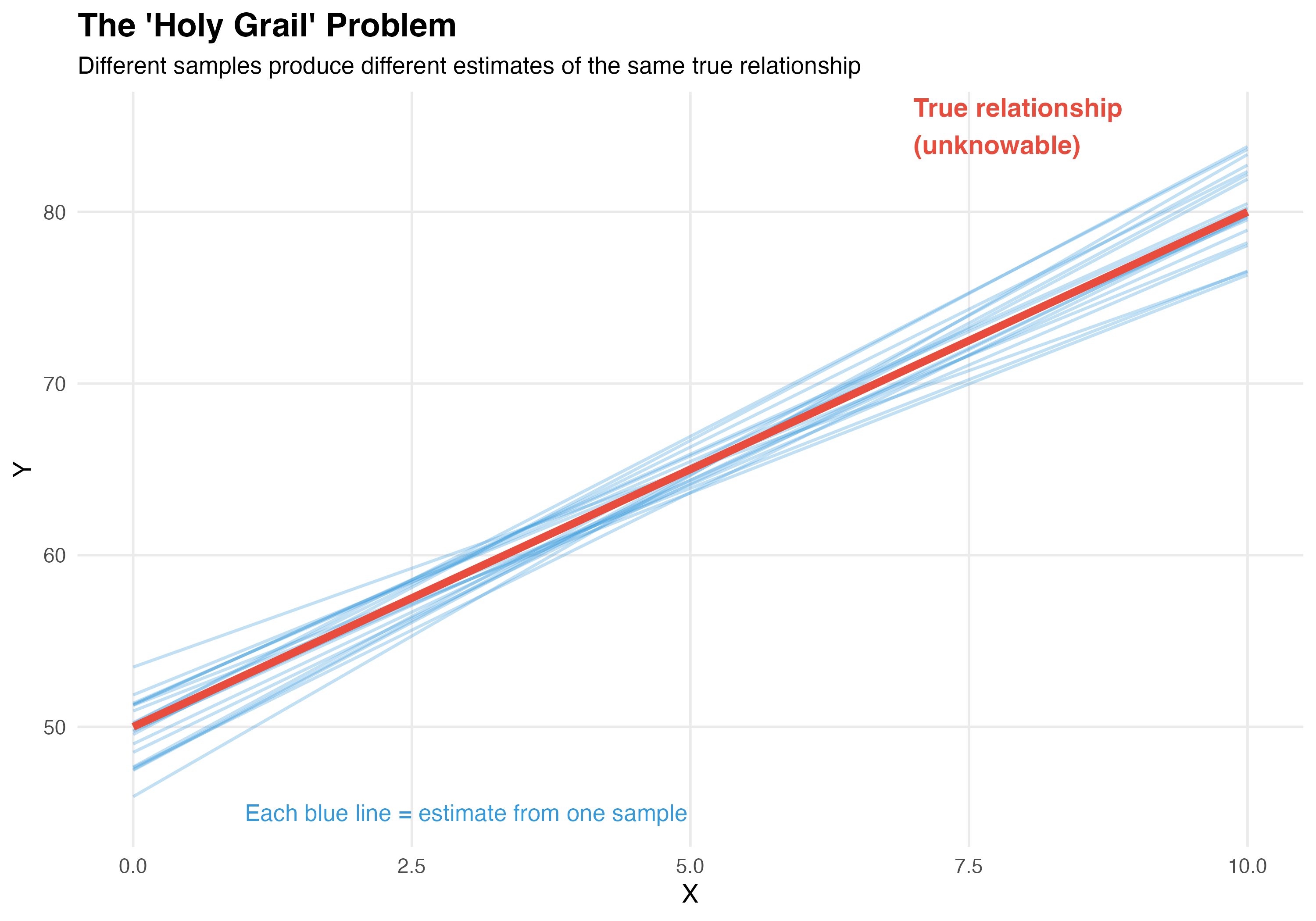

The “Holy Grail” Concept

Our estimates are just that: estimates of the true (unknown) parameters

Key insight:

- Red line = true relationship (unknowable)

- Blue line = our estimate from this sample

- Different samples → slightly different blue lines

- Standard errors quantify this uncertainty

Statistical Significance

The logic:

- Null hypothesis (H₀): β₁ = 0 (no relationship)

- Our estimate: β₁ = 0.02

- Question: Could we get 0.02 just by chance if H₀ is true?

t-statistic: How many standard errors away from 0?

- Bigger |t| = more confidence the relationship is real

p-value: Probability of seeing our estimate if H₀ is true

- Small p → reject H₀, conclude relationship exists

Part 4: Model Evaluation

How Good is This Model?

Two key questions:

- How well does it fit the data we used? (in-sample fit)

- How well would it predict new data? (out-of-sample performance)

These are NOT the same thing!

In-Sample Fit: R²

R² = 0.208

“21% of variation in income is explained by population”

Is this good?

- Depends on your goal!

- For prediction: Moderate

- For inference: Shows population matters, but other factors exist

R² alone doesn’t tell us if the model is trustworthy

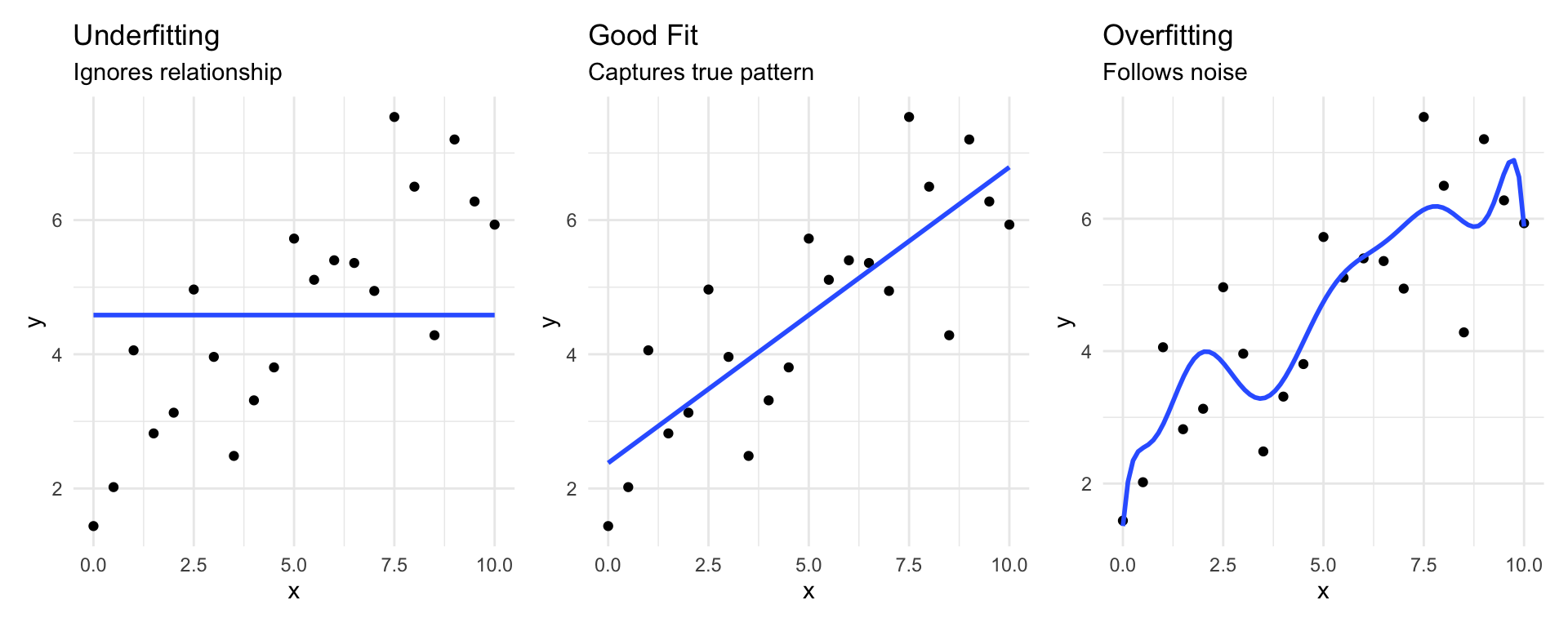

The Problem: Overfitting

Three scenarios:

- Underfitting: Model too simple (high bias)

- Good fit: Captures pattern without noise

- Overfitting: Memorizes training data (high variance)

Overfitting in Regression

The danger: High R² doesn’t mean good predictions!

Train/Test Split

Solution: Hold out some data to test predictions

set.seed(123)

n <- nrow(pa_data)

# 70% training, 30% testing

train_indices <- sample(1:n, size = 0.7 * n)

train_data <- pa_data[train_indices, ]

test_data <- pa_data[-train_indices, ]

# Fit on training data only

model_train <- lm(median_incomeE ~ total_popE, data = train_data)

# Predict on test data

test_predictions <- predict(model_train, newdata = test_data)Evaluate Predictions

# Calculate prediction error (RMSE)

rmse_test <- sqrt(mean((test_data$median_incomeE - test_predictions)^2))

rmse_train <- summary(model_train)$sigma

cat("Training RMSE:", round(rmse_train, 0), "\n")Training RMSE: 12893 Test RMSE: 9536 Interpreting RMSE

On new data (test set), our predictions are off by ~$9,500 on average. Is this level of error acceptable for policy decisions?

Cross-Validation

Better approach: Multiple train/test splits

Gives more stable estimate of true prediction performance

Cross-Validation in Action

library(caret)

# 10-fold cross-validation

train_control <- trainControl(method = "cv", number = 10)

cv_model <- train(median_incomeE ~ total_popE,

data = pa_data,

method = "lm",

trControl = train_control)

cv_model$results intercept RMSE Rsquared MAE RMSESD RsquaredSD MAESD

1 TRUE 12577.76 0.5643826 8859.865 5609.002 0.2997098 2238.042Key Metrics (Averaged Across 10 Folds)

- RMSE: Typical prediction error (~$12,578)

- R²: % of variation explained (0.564)

- MAE: Average absolute error (~$8,860) - easier to interpret

Part 5: Checking Assumptions

When Can We Trust This Model?

Linear regression makes assumptions. If violated:

- Coefficients may be biased

- Standard errors wrong

- Predictions unreliable

We must check diagnostics before trusting any model

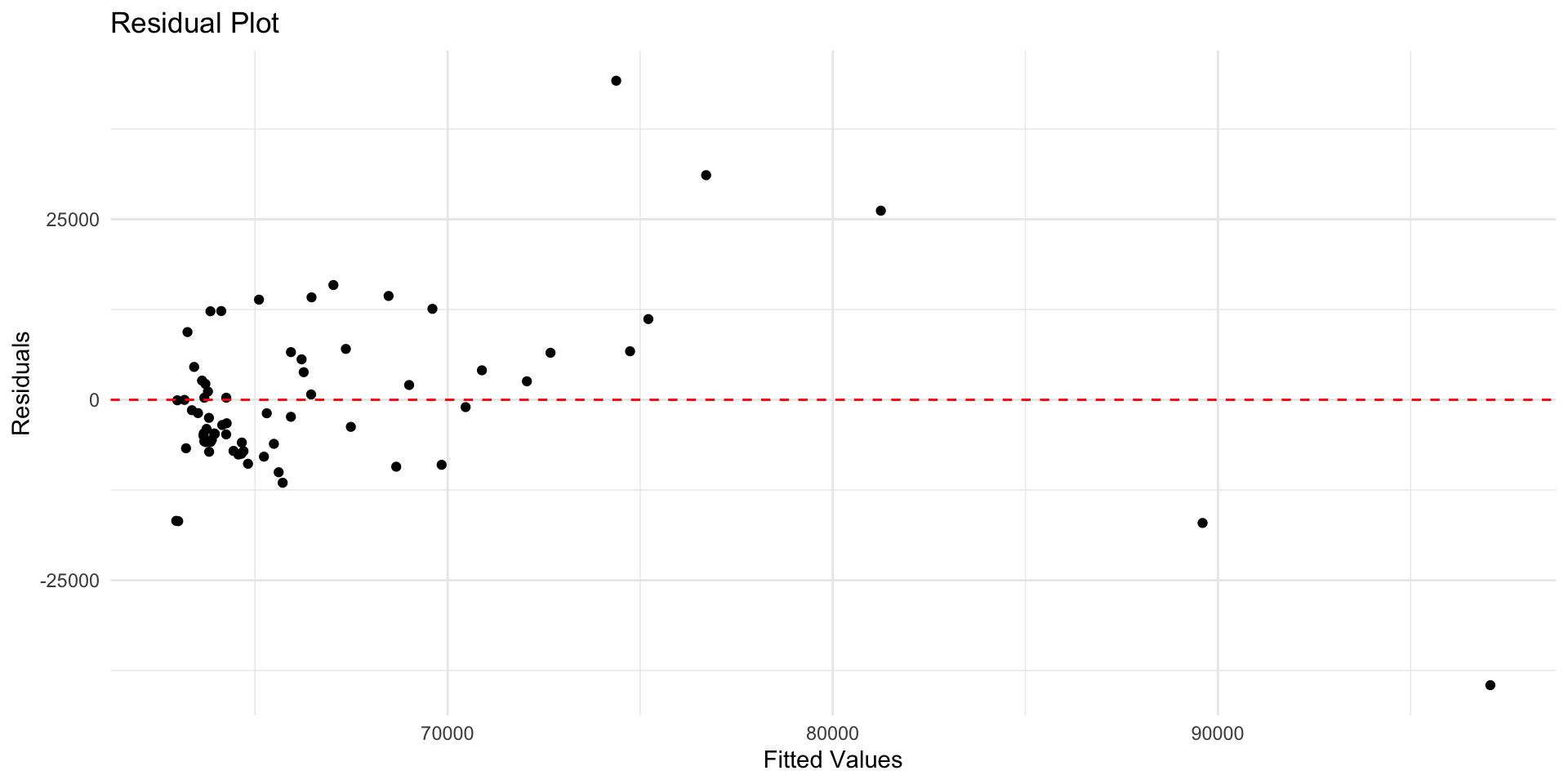

Assumption 1: Linearity

What we assume: Relationship is actually linear

How to check: Residual plot

Reading Residual Plots

Good

- Random scatter

- Points around 0

- Constant spread

Bad

- Curved pattern

- Model missing something

- Predictions biased

Why This Matters for Prediction

Linearity violations hurt predictions, not just inference:

- If the true relationship is curved and you fit a straight line, you’ll systematically underpredict in some regions and overpredict in others

- Biased predictions in predictable ways (not random errors!)

- Residual plots should show random scatter - any pattern means your model is missing something systematic

Assumption 2: Constant Variance

Heteroscedasticity: Variance changes across X

Impact: Standard errors are wrong → p-values misleading

What Heteroskedasticity Tells You

Often a symptom of model misspecification:

- Model fits well for some values (e.g., small counties) but poorly for others (large counties)

- May indicate missing variables that matter more at certain X values

- Ask: “What’s different about observations with large residuals?”

Example: Population alone predicts income well in rural counties, but large urban counties need additional variables (education, industry) to predict accurately.

Heteroskedasticity Visualized

Key Insight: Adding the right predictor can fix heteroscedasticity

Formal Test: Breusch-Pagan

studentized Breusch-Pagan test

data: model1

BP = 27.481, df = 1, p-value = 0.0000001587Interpretation:

- p > 0.05: Constant variance assumption OK

- p < 0.05: Evidence of heteroscedasticity

If detected, solutions:

- Transform Y (try

log(income)) - Robust standard errors

- Add missing variables

- Accept it (point predictions still OK for prediction goals)

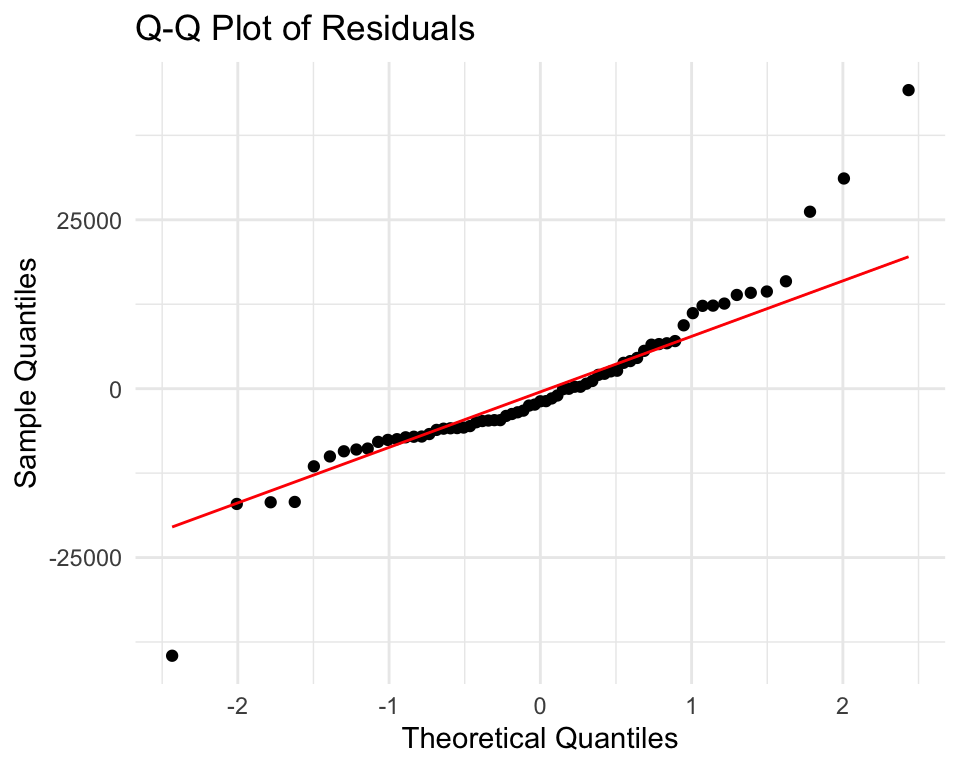

Assumption: Normality of Residuals

What we assume: Residuals are normally distributed

Why it matters:

- Less critical for point predictions (unbiased regardless)

- Important for confidence intervals and prediction intervals

- Needed for valid hypothesis tests (t-tests, F-tests)

Q-Q Plot

Assumption 3: No Multicollinearity

For multiple regression: Predictors shouldn’t be too correlated

Why it matters: Coefficients become unstable, hard to interpret

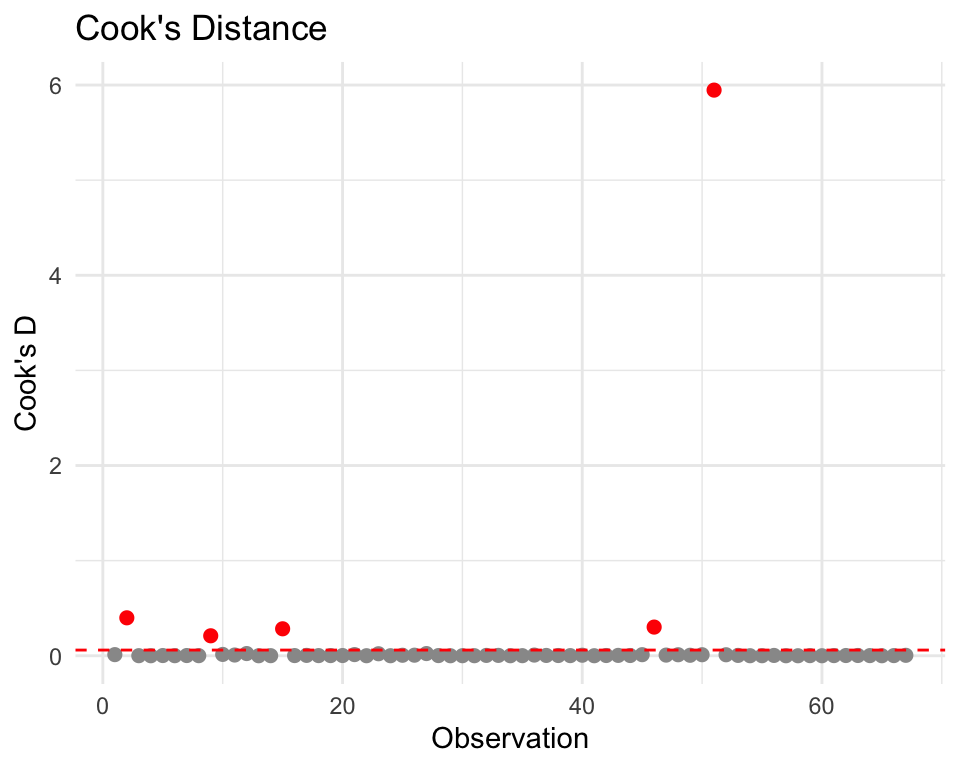

Assumption 4: No Influential Outliers

Not all outliers are problems - only those with high leverage AND large residuals

Visual Diagnostic

Identify Influential Points

# A tibble: 2 × 4

NAME total_popE median_incomeE cooks_d

<chr> <dbl> <dbl> <dbl>

1 Philadelphia County, Pennsylvania 1593208 57537 5.95

2 Allegheny County, Pennsylvania 1245310 72537 0.399Interpretation:

- Cook’s D > 4/n = potentially influential

- High leverage + large residual = pulls regression line

What To Do With Influential Points

Investigation Strategy

- Investigate: Why is this observation unusual? (data error? truly unique?)

- Report: Always note influential observations in your analysis

- Sensitivity check: Refit model without them - do conclusions change?

- Don’t automatically remove: They might represent real, important cases

For policy: An influential county might need special attention, not exclusion!

Connection to Algorithmic Bias

High-influence observations in demographic could represent marginalized communities or unique populations. Automatically removing them can erase important populations from analysis and lead to biased policy decisions.

Always investigate before removing!

Part 6: Improving the Model

Adding More Predictors

Maybe population alone isn’t enough:

Call:

lm(formula = median_incomeE ~ total_popE + percent_collegeE +

poverty_rateE, data = pa_data_full)

Residuals:

Min 1Q Median 3Q Max

-32939 -4473 -1098 3861 27672

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 60893.86796 1589.24122 38.316 < 0.0000000000000002 ***

total_popE 0.06657 0.03356 1.984 0.0517 .

percent_collegeE 0.04710 0.14916 0.316 0.7532

poverty_rateE -0.36503 0.07749 -4.711 0.000014 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 8610 on 63 degrees of freedom

Multiple R-squared: 0.5931, Adjusted R-squared: 0.5738

F-statistic: 30.61 on 3 and 63 DF, p-value: 0.000000000002485Log Transformations

If relationship is curved, try transforming:

# Compare linear vs log

model_linear <- lm(median_incomeE ~ total_popE, data = pa_data)

model_log <- lm(median_incomeE ~ log(total_popE), data = pa_data)

summary(model_log)

Call:

lm(formula = median_incomeE ~ log(total_popE), data = pa_data)

Residuals:

Min 1Q Median 3Q Max

-27231 -5780 -2118 3953 40638

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -4867 12374 -0.393 0.695

log(total_popE) 6276 1074 5.842 0.00000018 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 10760 on 65 degrees of freedom

Multiple R-squared: 0.3443, Adjusted R-squared: 0.3342

F-statistic: 34.13 on 1 and 65 DF, p-value: 0.0000001805Interpretation changes: Log models show percentage relationships

Categorical Variables

# Create metro/non-metro indicator

pa_data <- pa_data %>%

mutate(metro = ifelse(total_popE > 500000, 1, 0))

model3 <- lm(median_incomeE ~ total_popE + metro, data = pa_data)

summary(model3)

Call:

lm(formula = median_incomeE ~ total_popE + metro, data = pa_data)

Residuals:

Min 1Q Median 3Q Max

-28824 -6732 -2885 7672 26622

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 64924.857892 1659.821786 39.116 < 0.0000000000000002 ***

total_popE -0.005290 0.008047 -0.657 0.513257

metro 29865.529225 7319.309190 4.080 0.000127 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 10610 on 64 degrees of freedom

Multiple R-squared: 0.3718, Adjusted R-squared: 0.3522

F-statistic: 18.94 on 2 and 64 DF, p-value: 0.0000003456R creates dummy variables automatically

Summary: The Regression Workflow

- Understand the framework: What’s f? What’s the goal?

- Visualize first: Does a linear model make sense?

- Fit the model: Estimate coefficients

- Evaluate performance: Train/test split, cross-validation

- Check assumptions: Residual plots, VIF, outliers

- Improve if needed: Transformations, more variables

- Consider ethics: Who could be harmed by this model?

Key Takeaways

Statistical Learning:

- We’re estimating f(X), the systematic relationship

- Parametric methods assume a form (we chose linear)

Two purposes:

- Inference: understand relationships

- Prediction: forecast new values

Model evaluation:

- In-sample fit ≠ out-of-sample performance

- Beware overfitting!

Diagnostics matter:

- Always check assumptions

- Plots reveal what R² hides

🏆 Learning- Focused In-Class Challenge:

Best Predictive Model Competition

The Task

Predict median home value (B25077_001) for PA counties using any combination of predictors

Build the model with lowest 10-fold cross-validated RMSE

Available Predictors

challenge_data <- get_acs(

geography = "county",

state = "PA",

variables = c(

home_value = "B25077_001", # YOUR TARGET

total_pop = "B01003_001", # Total population

median_income = "B19013_001", # Median household income

median_age = "B01002_001", # Median age

percent_college = "B15003_022", # Bachelor's degree or higher

median_rent = "B25058_001", # Median rent

poverty_rate = "B17001_002" # Population in poverty

),

year = 2022,

output = "wide"

)Rules & Strategy

You can:

- Use any combination of predictors (time permitting, you can fetch more)

- Try log transformations:

log(total_popE) - Engineer new categorical features

- Remove influential outliers (but document which!)

You must:

- Use 10-fold cross-validation to report final RMSE

- Do a full diagnostic check (residual plot, Cook’s D, or Breusch-Pagan)

- Be ready to explain your model in 2 minutes

Hints

- Start simple (one predictor), check diagnostics

- Income and rent are probably highly correlated (multicollinearity!)

- Try log transformation if relationship looks curved

- Don’t forget to remove NAs:

na.omit(challenge_data)