t-statistic: How many standard errors away from 0?

Bigger |t| = more confidence the relationship is real

p-value: Probability of seeing our estimate if H₀ is true

Small p → reject H₀, conclude relationship exists

Model Evaluation

How well does it fit the data we used? (in-sample fit using R²)

How well would it predict new data? (out-of-sample performance)

Checking Assumptions: Plots reveal what R^2 hides

Assumption 1: Linear Relationship

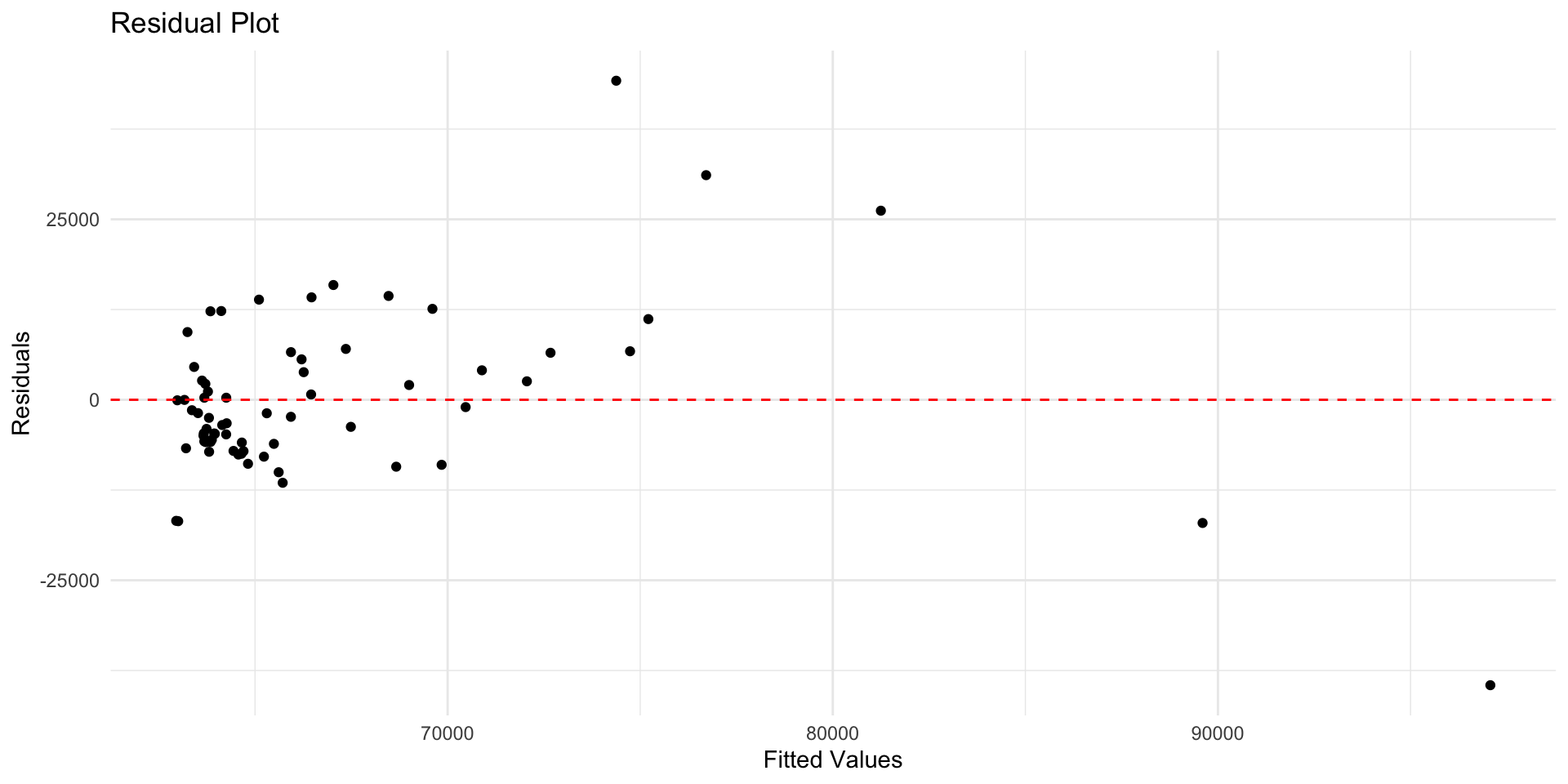

Check with Residual Plot

Residuals = observed − fitted. They’re your best proxy for the error term. Good models leave residuals that look like random noise.

Assumption 2: Constant Variance

Check heteroscedasticity (i.e. variance changes across X

Impact: standard errors are wrong -> p values are misleading

Assumption 3: Normality of Residuals

Check with Q-Q Plot (quantile-quantile plot) of residuals

Important for confidence & prediction intervals

Needed for valid hypothesis tests (t-test and F-test)

Assumption 4: No Multicollinearity

Coefficients become unstable and hard to interpret

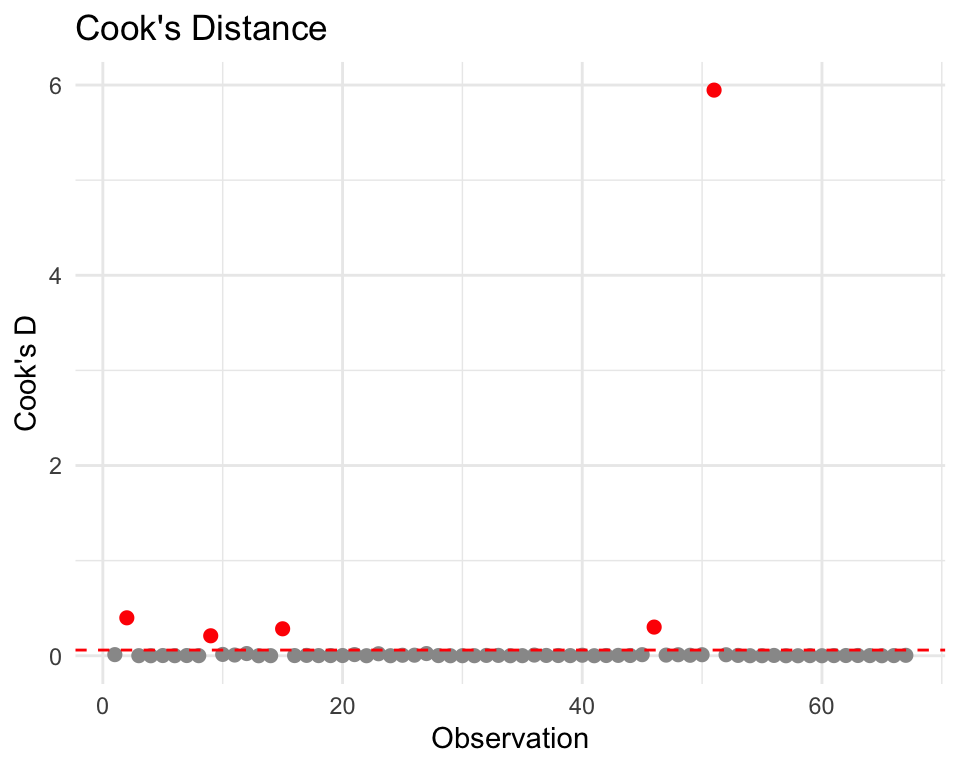

Assumption 5: No Influential Outliers

Influential Outliers: those with high leverage and large residuals

Visual Diagnostic using Cook’s Distance (Cook’s D)

Improving the Model

Adding more predictors

Log Transformations

Categorical Variables

Coding Techniques

Linear Regression Train/Test Split

Code

set.seed(123)n <-nrow(pa_data)# 70% training, 30% testingtrain_indices <-sample(1:n, size =0.7* n)train_data <- pa_data[train_indices, ]test_data <- pa_data[-train_indices, ]# Fit on training data onlymodel_train <-lm(median_incomeE ~ total_popE, data = train_data)# Predict on test datatest_predictions <-predict(model_train, newdata = test_data)

pa_data$residuals <-residuals(model1)pa_data$fitted <-fitted(model1)ggplot(pa_data, aes(x = fitted, y = residuals)) +geom_point() +geom_hline(yintercept =0, color ="red", linetype ="dashed") +labs(title ="Residual Plot", x ="Fitted Values", y ="Residuals") +theme_minimal()

Residuals vs Fitted

Goal: a random, horizontal band around 0. Residual plots should show random scatter - any pattern means your model is missing something systematic

Red flags:

Curvature → missing nonlinear term (try polynomials/splines or transform xxx).

Funnel/wedge shape → heteroskedasticity (use log/Box–Cox on yyy, weighted least squares, or robust SEs).

Clusters/bands → omitted categorical/group effects or interaction terms.

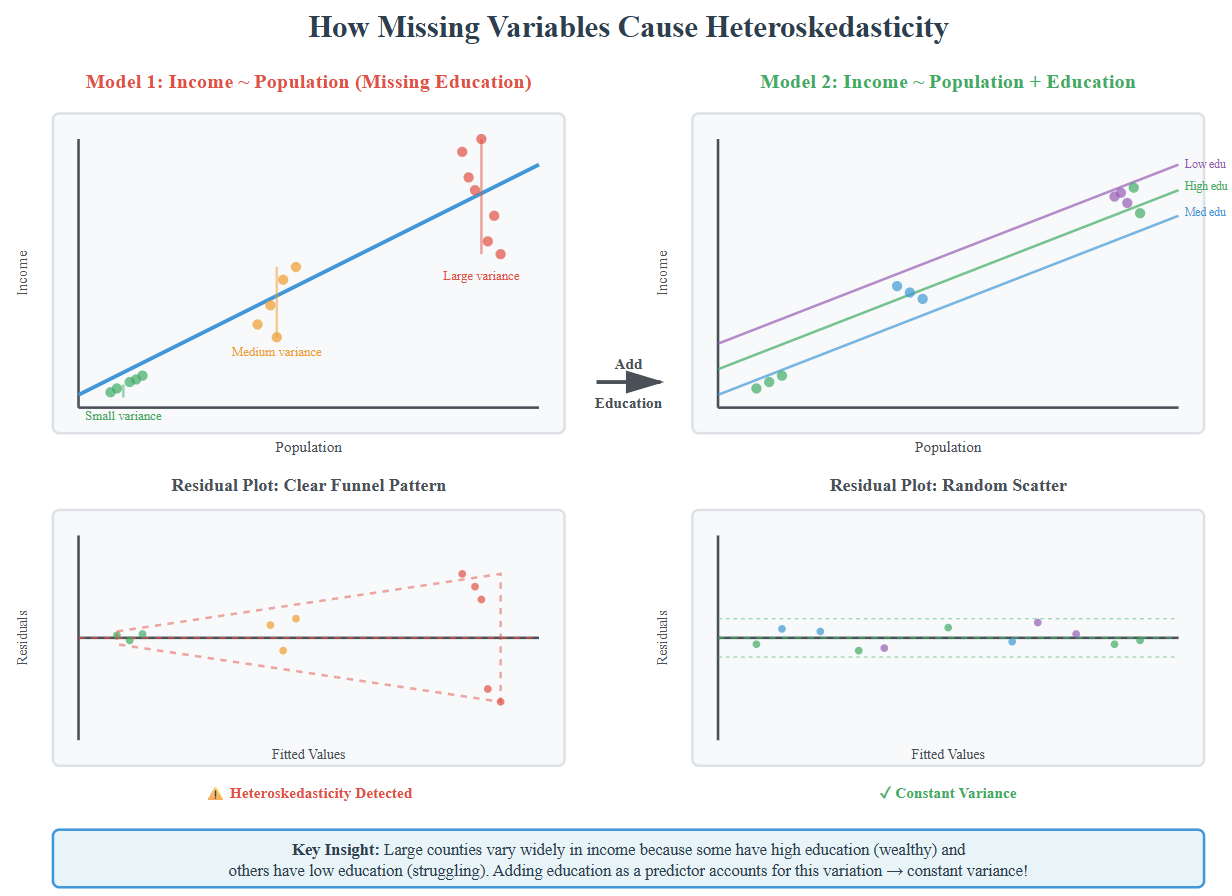

Constant Variance and Heteroskedacity

Heteroskedasticity is a condition in regression analysis where the variance of the error terms is not constant but changes as the value of one or more independent variables changes

Model fits well for some values (e.g., small counties) but poorly for others (large counties)

May indicate missing variables that matter more at certain X values

Ask: “What’s different about observations with large residuals?”

Formal Test: Breusch-Pagan

Code

library(lmtest) bptest(model1)

Interpretation:

p > 0.05: Constant variance assumption OK

p < 0.05: Evidence of heteroscedasticity

If detected, solutions:

Transform Y (try log(income))

Robust standard errors

Add missing variables

Accept it (point predictions still OK for prediction goals)

library(car)vif(model1) # Variance Inflation Factor# Rule of thumb: VIF > 10 suggests problems# Not relevant with only 1 predictor!

Influential Outliers – Cook’s D > 4/n

Questions & Challenges

I am also interested in learning more about non-parametric approaches in future weeks

Connections to Policy

It is important to understand the assumptions behind a model. For example, heteroskedasticity is often an indicator of model misspecification – it indicates missing variables that matter more at certain X values. Population alone predicts income well in rural counties, but large urban counties need additional variables (education, industry) to predict accurately.

Reflection

Excited to put these skills to the test with the midterm home price prediction challenge!